Table of contents

If there’s one constant in finances, it’s change. Cash flow changes, expense sheets change, and the costs of goods and services are in constant flux. When you add the global instability factors (inflation, conflicts, and pandemics, to name a few), it can all throw all your carefully laid plans into disarray.

Comprehensive, timely, and accurate financial reporting should help you make sense of it all, but things are a bit more complicated than that. Reporting brings its own challenges and, as is often the case, there’s no single template that will suit everyone. Regulatory compliance and inconsistencies further compound the issue, making lives harder for businesses and their accountants. Still, finance is one of the most monitored and reported operations, as Databox’s State of Business Reporting shows.

We have surveyed 34 businesses with varying specializations in order to shed some light on best practices for financial reporting. They talked about the reporting frequency, biggest challenges, and recent changes in financial monitoring and reporting.

This article will cover the following:

- How Often Companies Monitor and Report on Financial Performance

- Who’s in Charge of Preparing Financial Reports for Companies?

- How Has Financial Monitoring and Reporting Changed for Businesses in the Past 12 Months?

- Biggest Challenges in Financial Reporting

- 6 Best Practices for Accurate Financial Reporting

- How to Streamline Financial Reporting with Databox

How Often Companies Monitor and Report on Financial Performance

Establishing monitoring and reporting frequency is the first step to ensuring accurate and useful financial records. Most companies monitor their finances daily or weekly (around 70% total) while they usually (60%) report on a monthly basis. Weekly reporting comes in second at around 30%.

Gathering data at a granular level makes sense as you want to have as many data points as possible. This allows for better-informed decisions and more accurate reporting. Conversely, reporting that’s too frequent, can lack the “big picture” perspective and risks mistaking short-term changes for long-term trends. It can also simply clutter up your information stream and waste time on unnecessary reports. Still, they shouldn’t be too infrequent either, as that means you might miss some important signals.

Steve Elliott of Restoration1 insists that it’s important to maintain current financial statements. “Regularly reviewing your financial accounts is one of the best strategies to verify their accuracy. Creating a yearly balance sheet and income statement is a wonderful first step, but monthly updates to your financial records are considerably more effective.” Creating and examining financial statements can help you identify problem areas before they have a chance to disrupt your operations and becoming familiar with your balance sheet will allow you to spot any issues “Without this familiarity, you may not recognize when something has been misapplied or completely forgotten,” Eliott concludes.

Who is in Charge of Preparing Financial Reports for Companies?

A large majority of companies surveyed (over 70%) take care of financial reporting in-house. The rest outsource it to a consultant or an agency. It seems that businesses prefer to handle their own reporting most of the time.

That’s not surprising as financial reporting can be very sensitive and handling it within the company, ensures the right level of rigor and accountability.

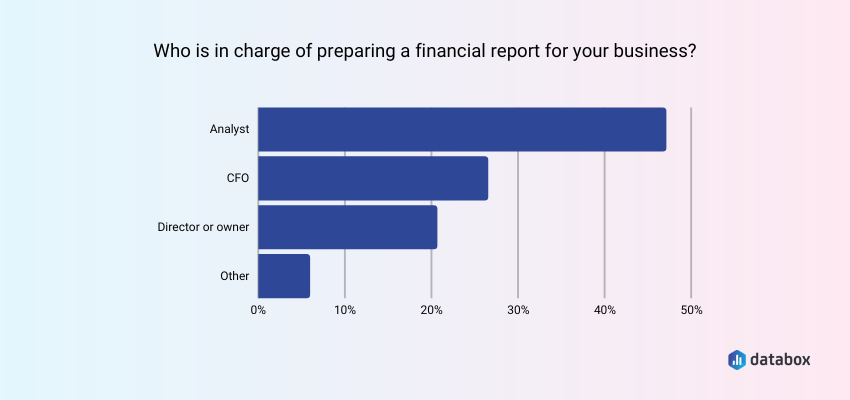

When it comes to preparing actual reports, analysts (whether they’re in-house, or external) shoulder the biggest share of the burden. Analysts are in charge of preparing a financial report for 47% of companies we surveyed. CFOs are the next in line at over 25%.

Finance specialists are clearly the preferred option for this kind of reporting. Only a quarter of surveyed companies pick a director or owner, or someone else to prepare a financial report.

How Has Financial Monitoring and Reporting Changed for Businesses in the Past 12 Months?

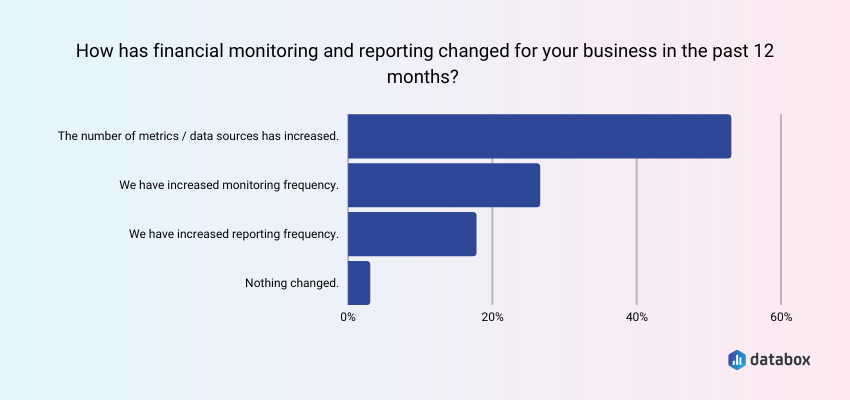

The last couple of years have certainly rattled every sector of the economy and finance is no exception. Over half of our respondents say that the biggest changes to financial reporting come in the form of the increased number of metrics and data sources. Roughly a quarter of them stated they have increased monitoring frequency and about 18% stated they have increased their reporting frequency. Only one respondent replied that nothing has changed.

It’s clear that businesses have focused even more attention on financial reporting than before. Every cent needs to be accounted for, and every decision weighed carefully, especially in times of economic instability where a wrong choice can make or break a company. Hence the need for more/better data sources and metrics and increased monitoring and reporting frequencies.

Pro Tip: How to Stay on Top of the Financial Health of Your Business

Do you own and manage a small business? Then you know how much of a struggle it can be to stay on top of the financial health of your business on a daily basis. Now you can pull data from QuickBooks and HubSpot’s CRM to track your key business metrics in one convenient dashboard, including:

- Open deals and deal amounts by pipeline stage. Get sales data directly from your HubSpot CRM and track deals, deal amounts, deal stages, and dates from your sales pipeline.

- Key financial data. Track gross profit margin, open invoices by amount and by customer, paid invoices, expenses, and income from QuickBooks.

Now you can benefit from the experience of our HubSpot CRM and QuickBooks experts, who have put together a plug-and-play Databox template that helps you monitor and analyze your key financial metrics. It’s simple to implement and start using it now!

You can easily set it up in just a few clicks – no coding required.

To set up the dashboard, follow these 3 simple steps:

Step 1: Get the template

Step 2: Connect your HubSpot and Quickbooks accounts with Databox.

Step 3: Watch your dashboard populate in seconds.

Biggest Challenges in Financial Reporting

Continuing from the previous point, it’s clear that data accuracy is the biggest challenge businesses face; this is confirmed by over 40% of our respondents. Process complexity is the next biggest challenge, distantly followed by dependency on consultants and analysts. Comparatively, very few respondents had trouble understanding and interpreting data.

A large number of data points and sources doesn’t necessarily mean all of them are accurate or relevant. In addition, the increase in the number of metrics and monitoring/reporting frequency, when combined with regulatory compliance requirements, exacerbates the issues with process complexity. Everything needs to be checked, double-checked, and cross-referenced. This, in turn, means that companies become more dependent on financial consultants and analysts, as they’re the only ones with the specialized knowledge needed to make sense of it all.

Related: How Small Businesses Deal with Inflation: Cost Cutting vs Spend Optimization

6 Best Practices for Accurate Financial Reporting

Financial overview reports help you better understand how your company is performing.

In order to ensure they give you as clear a picture as possible and attract potential investors, they need to be comprehensive, accurate, and understandable.

We asked our respondents for tips on how they ensure accurate and reliable financial reports. Here are some of the best practices they shared:

- Look to the cloud

- Use specialized software to extract and manage the data

- Ensure everyone understands the data

- Maintain transparency

- Log everything, all the time

- Focus on what really matters

Look to the cloud

Cloud systems allow for an unprecedented level of collaboration, ensuring data input and storage are more fluid and effective.

Manik Bhan of LinkGraph states that his company relies on a cloud-based accounting system, and every team member who is authorized to make any expenses has necessary access rights and reports expenses as they happen. “The system also catches the bank feeds and thus instantly catches the data on any income received. Moreover, it automatically assigns the right account and handles reconciliations. Thus, the system can update a P&L or a cash flow report at any time with the most recent data,” Bhan adds. This frees up a significant time for the accountant who can, in turn, use their expertise to interpret the data rather than manage it.

Use specialized software to extract and manage the data

It’s become almost impossible to run a business of any appreciable size without software assistance. This is especially true where finances are concerned. Accounting and data analytics systems help you make sense of the data, ensuring your financial reports are accurate and that your decision-making is based on solid information.

Eden Cheng of PeopleFinderFree focuses on data extraction. Since extracting financial data from multiple unstructured sources while maintaining quality and accuracy is a significant hurdle. He recommends using automated data extraction tools to manage high volumes of financial data. “These tools can help you to have a more detailed view of your company financials and reduce the amount of time you are spending manually reviewing reports, which in turn can often help to significantly streamline business operations in the process,” Cheng concludes.

Ensure everyone understands the data

“One of the best practices I use to ensure accurate and reliable financial reports is to make sure that my team has a thorough understanding of the company’s accounting policies,” says Rengie Wisper of Ever Wallpaper.

It’s difficult to argue with that position as it ensures that the team understands what they can report on, what they can’t report on, and why. This better understanding of the data allows them to interpret the data they have and make informed decisions based on it. Wisper adds, “When you have this kind of consistent knowledge among your team members, there’s less room for error or disagreement as to whether something should be reported or not. And when everyone is on the same page about what information needs to be reported, it makes it easier for them to find ways to improve performance.”

Related: 7 Data Analysis Questions to Improve Your Business Reporting Process

Maintain transparency

This is a good policy all around, not just when it comes to accuracy in financial reporting. Transparent reporting leads to better mutual understanding and accountability. If everyone who needs to have access to the data does, they’ll be able to check it for issues and ensure everyone is on the same page.

According to Melanie Mousson Expert Insurance Reviews, all managers at the company have access to the data. “Our analyst does an excellent job of interpreting and presenting the data, but giving all team leaders access to the data helps ensure that the reports are accurate. Each department has a budget and is required to track how each dollar is spent,” Mousson continues.

Keeping the spending public to members of leadership allows everyone to know where the budget is being spent and that knowledge and open communication can help identify inaccuracies in financial reports.

Log everything, all the time

A simple piece of advice, but an important one. Without keeping track of all expenses and incomes, you won’t have a solid foundation upon which to build your financial report. It will be difficult to verify the accuracy of the data, and you’ll probably have to spend a lot of time double-checking everything.

Consolidating all transactions is an excellent step towards having clean records. Caitly Parish of Cicinia believes that Consistent monthly transaction reconciliation is key to achieving accuracy in financial reporting. “Consistent monthly transaction reconciliation is one technique to produce financial reports on time. Every day, we keep track of and log my operational transactions. Similar to this, weekly ledger reconciliation saves a significant amount of time at the end of the month. I also employ technology automation to further streamline this task,” Parish concludes.

Ever Wallpaper’s Lily Will says that the company ensures financial reports are accurate and reliable by keeping all past transaction receipts available at all times. “In case there are events where we want to confirm the reliability of our reports, we are equipped to verify them. We do not need to deal with several processes to confirm. We just have to directly assess our documents. It is already acceptable to prove its accuracy.”

Focus on what really matters

It’s easy to drown in the sea of metrics and data sources. That’s why Tobias Liebsch, of Fintalent advocates for focusing on a smaller set of relevant ones. “Instead of having thousands of metrics, we focus on a very small set of KPIs (5-6) that have a direct impact on the business.”

Reporting that becomes too granular doesn’t really add direct value and there will always be more metrics to track. “So focus on the ones that actually drive the needle and make informed decisions faster to avoid analysis paralysis,” Liebsch concludes.

Streamline Financial Reporting with Databox

Financial reports aren’t just there for internal consumption. They’ll also be examined by both potential investors and government agencies. Therefore, achieving accuracy in financial reporting is incredibly important.

Unfortunately, it’s not exactly a simple process and, as we’ve seen, there are many challenges facing businesses when it comes to financial reporting. With the growing number of metrics to analyze, the whole thing can seem a bit overwhelming.

Fortunately, Databox can make it much easier. A business reporting tool allows you to collate and synthesize data simply and quickly with just a few clicks.

Thanks to Databox’s customizable Dashboards you can visualize all the important data points in one place. Your reports will be easy to understand and eye-catching, and they’ll minimize the chance of error, as they’ll draw information directly from your financial management tools.

Want to learn more? We’ve got you covered. Just sign up for a forever free Databox account and we’ll be with you every step of the way.